OpenWIS Financial Management

OpenWIS Association AISBL Treasurer, October 2017

This document pulls together the financial operating aspects of the OpenWIS association. This is intended as a supplement to the Articles of Association and Internal Rules. In the event of any discrepancy between the intentions noted in this document, meaning and governance shall be sought from the Articles of Association then the Internal Rules over this document.

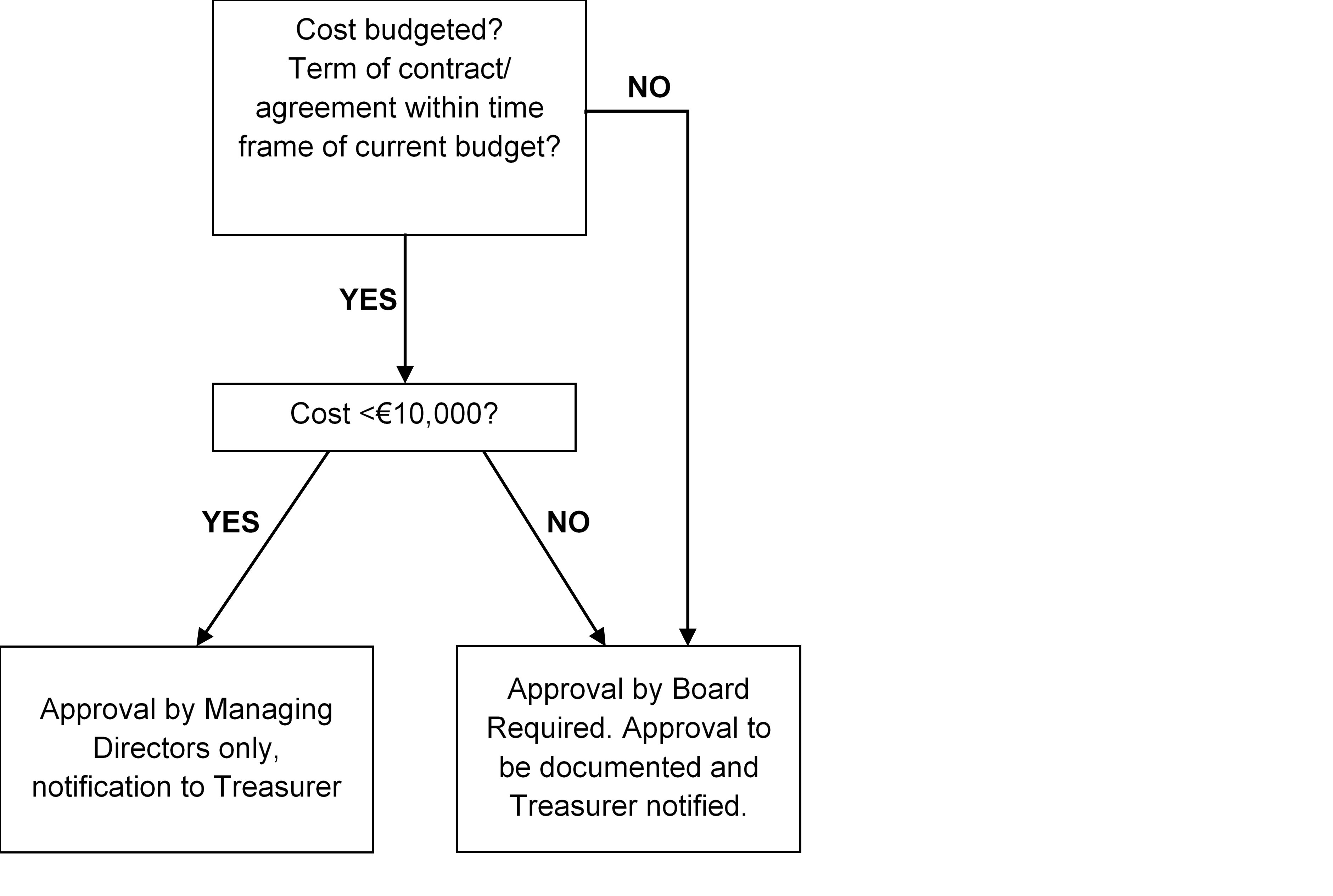

Approvals for Contracts/Agreements

This covers all costs to be incurred by OpenWIS whether directly as the contracting party or indirectly through the Members, Strategic Partners, and Associate Partners supporting the Association. Expenditure must be approved prior to incurring where required and due diligence should be taken when proceeding with transactions to ensure the association is getting value for money. Refer to the approvals process flow diagram for details.

{kind=link}

Invoice Administration

Invoices should be passed to the Treasurer who will ensure that sufficient approval is currently in place for the expenditure before approving the invoice for payment and proceeding with payment. Invoices shall be retained with approvals and evidence of payment (where appropriate) for accounting record purposes.

Alternative Currencies

The operating currency of the association is Euros. In the event that expenditure is incurred in other currencies, the prevailing exchange rate shall be used to determine the Euro value of any such transaction for accounting record purposes.

Payment Authorisation

All costs to be incurred must be authorised per above prior to payment. Authorisation for payment shall be completed in line with the requirements of the method of payment, e.g. 2 signatories. Payments processed through the bank account require dual signatory in line with best practice. The proxy holders are the president, vice president and treasurer. Any 2 from this group can complete the payment process.

Staff Costs

There are two main ways that OpenWIS Association AISBL could incur staff costs:

- Indirectly, where the individual is employed by a member organisation

- Directly by contracting with individual itself

In the case of an indirect arrangement, an agreement should be reached as to how these costs will be reimbursed, taking into account (but not limited to) frequency and total costs to be incurred and subsequently reimbursed by OpenWIS Association aisbl. The member organisation employing the individual is responsible for ensuring that all local tax and filing requirements are met. If the OpenWIS Association aisbl directly employs an individual, it is suggested that a local payroll bureau is engaged to ensure all local tax and filing requirements of the resident country of the individual are met. Consideration should any for any local pension, insurance or similar requirements when entering into a contract should also be noted.

In-kind contributions

As part of the operation of the Association, the partners contribute effort to the furthering and support of the aims of the association. This can be in the form of external spend with other suppliers or use of internal resources of the partners (e.g. staff time) to achieve this.

This is an in-kind transaction of the association and as such to the extent that this is measurable, the association should record this in their accounts. For Income & Expenditure Statement purposes, this is represented as a received income and a matching expense in the year.

In order to fulfil this obligation, the partners are required to submit an annual return to the Treasurer confirming the amount of in-kind costs they have incurred. Partners should consider what information they need to retain in year to be able to do this and raise any queries with the Treasurer. Returns should be made on the provided benefits-in-kind template.

In-kind contributions from individual Contributors, who are not part of a member or partner organisation, are considered unmeasurable. Therefore, they are not declared

Taxation

Corporation Tax & VAT

Non-profit associations may not pursue industrial and commercial activities. However, economic activities which promote the non-profit purpose of the association are allowed. Non-profit associations are in principle subject to tax on legal entities, not to corporation tax. They will not be taxed on subsidies, gifts, membership fees or any other income from its activities if they are of a non-profit making nature. But in purchasing goods and services they have to pay VAT

Employment Taxes

Refer to Staff Costs section.

Budget

The following requirements are specified in relation to budgets:

- Budgets are prepared annually for presentation at the Annual General Meeting.

- The budget will determine the level of membership contributions for the financial year.

- The budget shall reflect the estimated income and costs and shall be calculated in Euros.

- A reserve fund for unexpected developments or events should be maintained. To be determined at the Annual Meeting.

- Actual expenditure in year is compared against the budgeted amounts.

Annual Accounts

The following requirements are specified in relation to annual accounts:

- Annual Accounts must be communicated to Members not less than 30 days before the Annual Meeting.

- Accounting year runs from 1 January to 31 December

- The first financial year starts on the date of incorporation of the Organization and ends on 31 December 2015

- The Board shall prepare the annual accounts of the Organization in accordance with the Act and implementing legislation (as amended from time to time)

- The annual accounts shall be presented to the Annual Meeting for approval within six months following the closing of the financial year and, to this end, must be communicated to the Members at least thirty days prior to the date of such meeting

- The accounts must be accepted or rejected by the Board and a minute of this decision must be taken. In the event that the accounts are rejected, the reason for this decision must be recorded and the Treasurer must be instructed to prepare revised accounts as a matter of urgency.

Obligations under Belgian Law for Preparation of Accounts based on entity size:

The Belgian law distinguishes between three categories of associations, foundations and AISBL, with each category subject to specific filing obligations.

VERY LARGE Definition & Requirements:

Category Very Large are those that exceed an annual average of 100 paid workers, expressed in full-time equivalent or that meet two of the following three criteria:

- average paid workers (full time equivalent): 50

- total annual income, other than exceptional (excluding VAT): EUR 7,300,000

- balance sheet total: EUR 3.65 million.

Very Large organizations have the same accounting requirements as larger organizations and must also appoint a commissioner and a member of the Institute of Registered Auditors (IRE). (As adjusted by Royal Decree on the 25 August 2012)

LARGE Definition & Requirements:

Category Large are those that meet two of the following three criteria:

- average paid workers (full time equivalent): 5

- total annual income, other than exceptional (excluding VAT): EUR 312,500

- balance sheet total: EUR 1,249,500.

Large organizations must:

- keep accounts like a commercial companies with balance sheets, income statements and notes

- submit their accounts to the Registry of the Commercial Court and the National Bank within 30 days of their approval.

SMALL Definition & Requirements:

Category Small are all organisations not meeting the criteria of Large or Very Large organisations (examples: 2 employees and EUR 20,000 in revenues; or no workers and very little revenue).

Small organizations need only:

- keep simplified accounts with income statements and expenditure schedules

- submit their accounts to the Registry of the Commercial Court.

Note: accounts can be prepared in line with the requirements for large companies, this does not introduce a filing obligation with the National Bank.

The OpenWIS Association AISBL currently qualifies as a Small entity for filing purposes under Belgian Law, meeting only one of the criteria for Large organisations and this position is likely to continue. This position will need to be monitored annually.